Disclaimer: This Jupyter Notebook contains content generated with the assistance of AI. While every effort has been made to review and validate the outputs, users should independently verify critical information before relying on it. The SELENE notebook repository is constantly evolving. We recommend downloading or pulling the latest version of this notebook from Github.

Boosting in Machine Learning — Overview¶

Boosting is one of the most influential and successful ensemble learning paradigms in modern machine learning. The central idea is to combine a sequence of relatively simple models, often referred to as weak learners, into a single, highly accurate predictive model. Unlike bagging methods, which train individual models independently and aggregate their predictions, boosting constructs learners sequentially, with each new model focusing on the mistakes made by the current ensemble. This iterative error-correction mechanism enables boosting methods to achieve remarkable predictive performance across a wide range of classification and regression tasks.

This notebook introduces the fundamental concepts underlying boosting and provides an overview of the most important boosting strategies. We begin with AdaBoost, one of the earliest and most influential boosting algorithms, which improves performance by repeatedly reweighting the training data so that incorrectly predicted examples receive greater emphasis in subsequent iterations. We then turn our attention to Gradient Boosting Machines (GBMs), a more general framework in which each new learner is trained to predict the residual errors — or more generally, the gradients of a loss function — of the current ensemble. This perspective connects boosting to optimization and forms the foundation of many modern boosting algorithms.

Building on the basic GBM framework, the notebook also discusses the key innovations introduced by several state-of-the-art boosting libraries. In particular, we examine how XGBoost improves predictive performance and computational efficiency through regularization and second-order optimization, how LightGBM scales boosting to large datasets through efficient tree construction techniques, and how CatBoost addresses challenges associated with categorical features through ordered target encoding, ordered boosting, and oblivious trees. These methods illustrate how the core principles of boosting have been refined and extended to address practical challenges encountered in real-world machine learning applications.

Learning about boosting methods is particularly important because they consistently rank among the best-performing algorithms for structured (tabular) data. In many practical classification and regression problems, boosting models achieve state-of-the-art results and often serve as strong baseline models against which other approaches are compared. Understanding the principles, strengths, limitations, and key innovations of modern boosting algorithms is therefore an essential skill for anyone seeking to apply machine learning effectively to real-world data.

Setting up the Notebook¶

This notebook does not contain any code, so there is no need to import any libraries.

Preliminaries¶

Before checking out this notebook, please consider the following:

The focus of the notebook is to provide an overview of popular boosting techniques. The notebook makes no claim to be comprehensive.

The different boost strategies are covered in such a way to highlight their individual key contributions, including using illustrative examples. While the notebook includes some mathematical foundations, many (implementation) details are beyond the its scope

As most practical boosting techniques use Decision Trees as their base learners, a solid knowledge about Decision Trees is recommended.

This notebook assumes a basic understanding of calculus and concepts of derivatives and partial derivatives.

Motivation¶

Ensembles Learning — Quick Recap¶

Individual machine learning models are often constrained by the bias–variance tradeoff, which limits their predictive performance. Models with high bias, such as simple linear classifiers, make strong assumptions about the underlying data and may underfit, resulting in systematic prediction errors. Conversely, highly flexible models can achieve low bias but often exhibit high variance, meaning that their predictions are sensitive to fluctuations in the training data and may not generalize well to unseen examples. As a result, a single model typically struggles to simultaneously achieve low bias, low variance, and high predictive accuracy.

Ensemble learning addresses these limitations by combining the predictions of multiple models into a single, more robust predictor. The central idea is that different models are likely to make different errors; by aggregating their predictions, these errors can partially cancel out, leading to improved generalization performance. Depending on the ensemble strategy, combining multiple learners can reduce variance, reduce bias, or leverage the complementary strengths of diverse models. Consequently, ensemble methods often achieve higher accuracy, greater stability, and better robustness than individual models. Some of the most popular ensemble strategies include:

Voting & Averaging. Voting and averaging are simple ensemble strategies that combine the predictions of multiple models to produce a final prediction. The main advantage of these approaches is their simplicity, ease of implementation, and ability to improve predictive performance by reducing variance and mitigating the impact of individual model errors. However, their effectiveness depends on the diversity and quality of the constituent models; if the models make similar mistakes or if several weak models are included, the ensemble may provide only limited improvement. Furthermore, voting and averaging treat model interactions implicitly and cannot learn optimal combinations of model predictions.

Bagging (Bootstrap Aggregating). This ensemble learning strategy trains multiple instances of the same base learner on different bootstrap samples of the training data, where each sample is generated by randomly drawing observations with replacement. The predictions of these models are then combined through voting for classification or averaging for regression. The primary advantage of bagging is its ability to reduce variance and improve model stability, making it particularly effective for high-variance learners such as decision trees; Random Forest is a well-known example of a bagging-based method. Additionally, because the models are trained independently, bagging can be parallelized efficiently. However, bagging generally does not reduce bias, meaning that if the base learner systematically underfits the data, the ensemble is unlikely to achieve substantial improvements.Furthermore, the performance gains diminish when the individual models are highly correlated and therefore make similar prediction errors.

Stacking. Stacking (or stacked generalization) combines the predictions of multiple base models by training a second-level model, known as a meta-learner, to learn how best to combine their outputs. Instead of simply averaging or voting, the meta-learner uses the predictions of the base models as input features and learns patterns in their strengths and weaknesses, allowing it to produce more accurate final predictions. The main advantage of stacking is its ability to leverage the complementary strengths of diverse models, often achieving higher predictive performance than any individual model or simpler ensemble methods. However, stacking is more complex to implement and train, requiring careful use of cross-validation to avoid information leakage and overfitting. It is also computationally more expensive than methods such as bagging or voting, as multiple models and an additional meta-model must be trained.

Boosting. This strategy builds a strong predictive model by sequentially training a series of weak learners, where each new learner focuses on correcting the errors made by its predecessors. Unlike bagging, which trains models independently, boosting assigns greater importance to difficult examples or residual errors, allowing the ensemble to progressively improve its predictions. This approach can substantially reduce bias and often achieves state-of-the-art performance on tabular datasets, as demonstrated by algorithms such as AdaBoost, Gradient Boosting, XGBoost, and LightGBM. However, because the models are trained sequentially, boosting is more computationally expensive and less amenable to parallelization than bagging. Additionally, if not properly regularized, boosting can be sensitive to noise and outliers and may overfit the training data, particularly when too many learners are added.

While Voting & Averaging, Bagging, Stacking, and Boosting are among the most widely used ensemble learning strategies, they do not encompass the full range of ensemble approaches. Other notable methods include Blending, which is a simplified variant of stacking that uses a holdout validation set to train a meta-learner, and Mixture of Experts (MoE), which employs a gating mechanism to dynamically select or weight specialized models based on the input. Additional approaches such as deep ensembles, snapshot ensembles, and Bayesian model averaging further demonstrate the diversity of ensemble techniques. Despite their differences, all ensemble methods share the common goal of combining multiple models to achieve better predictive performance, robustness, and generalization than could be obtained from a single model alone.

Boosting — Basic Idea¶

Among ensemble learning strategies, boosting stands out due to two distinctive characteristics. First, it employs sequential learning of dependent model, where models are trained one after another, with each new model focusing on correcting the errors made by the previous ones. This contrasts with methods such as bagging and voting, where models are trained independently. Second, boosting is closely associated with the use of weak learners, which are simple models that perform only slightly better than random guessing. By iteratively combining many such weak learners, boosting constructs a strong predictive model that can achieve high accuracy and effectively reduce bias, making it one of the most influential ensemble learning paradigms.

Sequential Learning¶

A common characteristic of many ensemble learning strategies is that the constituent models are trained independently of one another. In voting and averaging ensembles, each model is trained separately and their predictions are simply combined during inference. Similarly, bagging methods train multiple models independently on different bootstrap samples of the data, allowing their predictions to be aggregated afterward. Stacking also largely follows this paradigm, as the base models are trained independently and only interact through the subsequent meta-learner that combines their predictions. One of the major advantages is that they naturally support parallelized training. As a result, independent-model ensembles often offer shorter training times and better scalability when sufficient computational resources are available.

In contrast, boosting involves the training of dependent models. In a nutshell, the basic intuition behind boosting is that instead of trying to build one perfect model, build many simple models sequentially, where each new model focuses on correcting the mistakes made by the previous ones. To give a simple analogy, consider a group of students preparing for a group quiz using past years' papers — note that they will take the quiz together and not independently. Instead of all students learning all quiz topics, boosting proposes the following approach

- Student 1 attempts all questions from the past years' papers and then checks which one he or she got wrong.

- Student 2 attempts all (or maybe just some!) questions but focuses more on the ones that Student 1 got wrong.

- Student 3 attempts all (or maybe just some!) questions but focuses more on the ones that Student 1 and Student 2 got wrong.

- ...

Then, when taking the quiz, all students attempt all quiz questions and combine all their answers, giving more weight to the students who performed better. Under basic assumption (discussed later), the group can achieve much better performance than any individual student. In this analogy, the students are the models (or learners) that try to improve on the mistakes of the previous model.

Note that this analogy best describes the idea behind AdaBoost, one of the earliest boosting algorithms that became widely used and practical; we will cover AdaBoost later in more detail. While other boosting methods rely on some other mechanisms, the overall idea remains the same: the sequential training of dependent models where subsequent models aim to improve on the errors of previous models. One obvious limitation, compared to other ensemble learning strategies, is that with boosting the individual models can no longer be trained in parallel.

Weak Learners¶

Most ensemble learning methods start by training each individual model to achieve the highest predictive accuracy possible on its own. The intuition is that if each model is already a high-quality predictor, then combining their predictions through averaging, voting, or stacking can further improve performance by reducing variance and increasing robustness. Models trained to perform as well as possible individually are known as strong learners. Examples include the deep decision trees used in Random Forests or complex neural networks used in model ensembles. The ensemble's benefit comes primarily from combining multiple strong but diverse predictors.

Boosting is somewhat different: instead of combining independently trained strong learners, it deliberately uses weak learners — models that perform only slightly better than random guessing — and combines them sequentially so that each learner corrects the mistakes of the previous ones (see above). The ensemble itself becomes the strong learner!

This idea of weak learners may seem counter-intuitive since the obvious argument arises: "If weak learners are good, then strong learners should be even better." However, combining strong learners in a boosting architecture actually causes the whole system to break down mathematically and computationally. Keep in mind that in boosting, the ensemble is supposed to do the heavy lifting; the goal is not for each individual model to solve the entire problem but instead (reflecting the analogy above):

- Learner 1 captures the most obvious patterns.

- Learner 2 corrects the remaining mistakes.

- Learner 3 corrects what's still wrong.

- ...

In short, each learner only needs to contribute a small improvement. Using a very strong learner at each step — to use the analogy again — is like requiring all students to perfectly study all the topics, and students may make only tiny corrections to other students' already good solutions. In practical settings, this is often unnecessarily wasteful. Boosting does not just prefer weak learners, it practically requires them. If you try to use strong learners in a boosting model, the following two main problems (are very likely to) occur:

No "information" for subsequent models. Model Recall that boosting sequentially trains dependent models on the errors of the previous models. If, say, Model 1 is already a strong learner, it will aggressively fit the training data, potentially achieving a very low training error — keep in mind that this does not mean that this model is guaranteed to generalize well! Because Model 1 leaves almost no error, there is no signal left for Model 2 to learn from. The target it is trying to predict is just random noise and tiny statistical anomalies. A strong first model effectively starves the rest of the sequence, making the "sequential teamwork" aspect of boosting entirely useless.

Aggressive Overfitting (The Variance Explosion). The ultimate goal of any machine learning model is to generalize well to unseen data. In machine learning, we manage this using the Bias-Variance Tradeoff: In general, strong learners have low bias (they are smart) but high variance (they overfit easily and are erratic), whereas weak learners have high bias (they are too simple) but low variance (they are highly stable and do not overfit). Boosting is explicitly designed to reduce bias. It takes high-bias, stable models and bends them iteration-by-iteration to fit the data. If you chain strong, high-variance models together sequentially, their variances do not cancel out, but they compound. Model 2 will overfit to the tiny errors of Model 1, and Model 3 will overfit to the even weirder errors of Model 2. Within 3 or 4 iterations, you will have an incredibly complex, erratic model that memorizes the training data perfectly but fails completely on new data.

In principle, almost any supervised learning model can be used as a weak learner in a boosting framework. Since boosting only requires a model that can capture some aspect of the remaining error, base learners may range from linear models and rule-based classifiers to neural networks and kernel methods. In practice, however, Decision Trees are by far the most popular choice. Shallow trees are computationally efficient, naturally capture non-linear relationships and feature interactions, and can be trained on weighted data or residuals with little modification. Moreover, they are flexible enough to learn meaningful corrections at each boosting iteration while remaining simple enough to avoid overfitting. As a result, most modern boosting algorithms — including Gradient Boosting Machines (GBMs), XGBoost, LightGBM, and CatBoost — use Decision Trees as their default base learners.

Side note: A related concept can be found in Mixture of Experts (MoE) architectures and similar modular machine learning approaches. In these systems, multiple specialized components, often referred to as experts, learn to handle a subset of the overall task, while a gating mechanism determines which expert(s) should contribute to a particular prediction. In this sense, individual experts may resemble weak learners because they are not intended to solve the entire problem on their own. However, there is an important distinction: in MoE architectures, the experts are typically subcomponents of a single, jointly trained model, whereas in boosting, weak learners are independent models that are trained sequentially and then combined into an ensemble. Thus, while both approaches rely on the idea of combining multiple specialized predictors, the term weak learner in the context of boosting specifically refers to individual models rather than modules within a larger model.

Outline: Boosting Strategies¶

As already mentioned, boosting algorithms are generally agnostic to the choice of base learner. In principle, any learning algorithm that performs slightly better than random guessing can be used as a weak learner within a boosting framework. For example, linear classifiers, rule-based classifiers, and even neural networks can serve as base learners. The role of boosting is to combine many such weak learners into a strong ensemble by training them sequentially and encouraging each new learner to focus on samples that previous learners found difficult to classify.

In practice, however, Decision Trees have become the preferred choice of base learners for most boosting algorithms. Decision trees naturally handle both numerical and categorical features, require little data preprocessing, and can capture nonlinear relationships and feature interactions. The trees used as weak learners are often intentionally kept very simple and shallow to prevent overfitting. Such shallow trees are commonly referred to as Decision Stumps, which typically consist of only very few splits or potentially only a single split. Although each Decision Stump is a very weak classifier on its own, the combination of many stumps can produce a highly accurate and robust predictive model.

Therefore, throughout the rest of the notebooks, we assume Decision Trees — or rather Decision Stumps — as the base learner for the all boosting strategies we will cover.

Reweighting the Data (AdaBoost)¶

AdaBoost (Adaptive Boosting) was one of the first boosting algorithms to become widely popular and successful in practice. Introduced by Freund and Schapire in the 1990s, AdaBoost demonstrated that combining many weak learners could produce a highly accurate classifier. Its simplicity, strong theoretical foundations, and impressive empirical performance made it a cornerstone of ensemble learning and inspired many subsequent boosting methods.

Basic Idea: Sample Weights¶

The key idea behind AdaBoost is to maintain a weight for each training sample that reflects how difficult that sample has been to classify correctly. Initially, all training samples are assigned equal weights. After each weak learner is trained, the weights of misclassified samples are increased, while the weights of correctly classified samples are decreased. As a result, subsequent learners focus more attention on samples that previous learners struggled with. The final prediction is obtained by combining the predictions of all weak learners through a weighted vote, where learners with lower classification error receive greater influence. By iteratively emphasizing hard-to-classify samples, AdaBoost gradually constructs a strong classifier from a sequence of weak classifiers.

To illustrate this idea, let's consider the following example dataset of a classification task with $N=10$ training samples to predict if bank customers will default on their credit.

| ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | DEFAULTED |

|---|---|---|---|---|

| 1 | 24 | Single | 28,000 | Yes |

| 2 | 45 | Married | 92,000 | No |

| 3 | 31 | Single | 55,000 | Yes |

| 4 | 52 | Divorced | 38,000 | No |

| 5 | 29 | Married | 120,000 | No |

| 6 | 41 | Widowed | 47,000 | No |

| 7 | 22 | Single | 21,000 | Yes |

| 8 | 36 | Married | 75,000 | No |

| 9 | 58 | Divorced | 33,000 | Yes |

| 10 | 27 | Single | 65,000 | Yes |

We now attached a weight to each sample. Since AdaBoost requires that all weights sum up to $1$ and at the beginning we have not information which samples might be easier or harder to classify correctly, we initialize weights equally, i.e., $w_i = 1/N$ for the $i$-th sample; with $N=10$, we get $w_i = 0.1$ for all samples. We add this weight as a column to the table below, but keep in mind that this weight is not a new feature!

| Weight wi | ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | DEFAULTED |

|---|---|---|---|---|---|

| 0.1 | 1 | 24 | Single | 28,000 | Yes |

| 0.1 | 2 | 45 | Married | 92,000 | No |

| 0.1 | 3 | 31 | Single | 55,000 | Yes |

| 0.1 | 4 | 52 | Divorced | 38,000 | No |

| 0.1 | 5 | 29 | Married | 120,000 | No |

| 0.1 | 6 | 41 | Widowed | 47,000 | No |

| 0.1 | 7 | 22 | Single | 21,000 | Yes |

| 0.1 | 8 | 36 | Married | 75,000 | No |

| 0.1 | 9 | 58 | Divorced | 33,000 | Yes |

| 0.1 | 10 | 27 | Single | 65,000 | Yes |

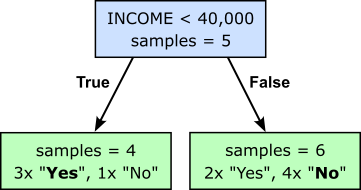

This is the starting point to train our first learner. Let's assume that we have trained a Decision Stump with a single split and got the following result:

If we use this Decision Stump to classify all training samples, we see that we make $3$ misclassifications:

- ID 4 gets misclassified as "Yes" since the majority of customers with an annual income less than $40k$ default on their credit.

- ID 3 and ID 10 get misclassified as "No" since the majority of customers with an annual income more than $40k$ will not default on their credit.

We can also show this outcome by color coding the data table with green rows reflecting correct classifications and red rows reflecting misclassification.

| Weight wi | ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | DEFAULTED |

|---|---|---|---|---|---|

| 0.1 | 1 | 24 | Single | 28,000 | Yes |

| 0.1 | 2 | 45 | Married | 92,000 | No |

| 0.1 | 3 | 31 | Single | 55,000 | Yes |

| 0.1 | 4 | 52 | Divorced | 38,000 | No |

| 0.1 | 5 | 29 | Married | 120,000 | No |

| 0.1 | 6 | 41 | Widowed | 47,000 | No |

| 0.1 | 7 | 22 | Single | 21,000 | Yes |

| 0.1 | 8 | 36 | Married | 75,000 | No |

| 0.1 | 9 | 58 | Divorced | 33,000 | Yes |

| 0.1 | 10 | 27 | Single | 65,000 | Yes |

AdaBoost now computes several values needed to update the weights $w_i$. First, it computes the total error $\epsilon$ for the weak learner as the sum of the current weights of all the misclassified samples. With $3$ misclassifications and all initial weights being $0.1$, we get a total error of $\epsilon = 0.3$. Next, based on the total error, AdaBoost computes the so-called "amount of say" $\alpha$ which measures how much influence a weak learner has on the final ensemble prediction. Weak learners that make fewer mistakes receive a larger amount of say, while learners that perform poorly receive a smaller amount of say. For a binary classification task — which we have here — the amount of say for a weak learner is computed as:

Plugging in the total error of $0.3$ we get an amount of say for this weak learner of $\alpha = 0.42$. Based on $\alpha$, AdaBoost now updates the weights of all samples. More specifically, AdaBoost reduces the weight of correctly classified samples, and increases the weight of wrongly classified samples using the following update rule:

This update rule does generally not result in new weights that will sum up to $1$. However, since this is required for AdaBoost to perform correctly, the last step is therefore to normalize all weights using $w_{i} = w_i/\sum_{i}^{N}w_i$. Thus, after all these steps, we get the new weights for all data samples as shown in the table below (note that the weights do not exactly sum up to $1$ due to limited precision).

| Weight wi | ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | DEFAULTED |

|---|---|---|---|---|---|

| 0.071 | 1 | 24 | Single | 28,000 | Yes |

| 0.071 | 2 | 45 | Married | 92,000 | No |

| 0.167 | 3 | 31 | Single | 55,000 | Yes |

| 0.167 | 4 | 52 | Divorced | 38,000 | No |

| 0.071 | 5 | 29 | Married | 120,000 | No |

| 0.071 | 6 | 41 | Widowed | 47,000 | No |

| 0.071 | 7 | 22 | Single | 21,000 | Yes |

| 0.071 | 8 | 36 | Married | 75,000 | No |

| 0.071 | 9 | 58 | Divorced | 33,000 | Yes |

| 0.167 | 10 | 27 | Single | 65,000 | Yes |

Notice how the weights of misclassified samples increased, and the weights of correctly classified samples decreased. The whole idea of AdaBoost is to use these weights in such a way that subsequent learners pay more attention to misclassification to improve on the errors of previous learners. How this is done in detail will be covered in the next section.

Incorporating Weights¶

So far, we have seen how AdaBoost uses the accuracy of a learn in terms of its misclassification to update the weights, i.e., increasing the weights of misclassified samples and decreasing the weights of correctly classified samples. However, we still need to address how the weights actually affect the training process. Recall that the general idea behind AdaBoost — and boosting in general — is that subsequent learners pay more attention to "bad" samples, that is, samples that have been (frequently) misclassified. Now that we have a way to identify bad samples using the sample weights, we now need a way to formalize the idea of learners to "pay more attention" to bad samples. There are two fundamental approaches for this: incorporate the weights into the loss or generated bootstrap samples based on the sample weights.

Weighted Loss¶

When training a supervised machine learning model, the loss function is the means to quantify how good or bad the current model is performing. Normally, each training sample contributes equally to the total loss. Thus, assuming $N$ training samples, each sample contributes $1/N$ to the total loss. In contrast, in a weighted setup such as AdaBoost, each data point $i$ is assigned an individual weight vector, $w_i$, and the loss function is modified so that the penalty for misclassifying point $i$ is multiplied by $w_i$:

where $\mathcal{L}(y_i, \hat{y}_i)$ is the sample loss quantifying the loss by computing the difference between the predicted value and the ground truth value of the $i$-th sample (e.g., the Mean Sqared Error (MSE) for regression tasks or the Cross-Entropy loss for classification tasks).

When training an AdaBoost ensemble model with Decision Trees as base learners, the weighted loss is incorporated at the most fundamental level of the tree's construction: the splitting criterion (such as Gini Impurity or Entropy). Instead of just counting the number of misclassified samples to determine the best split, the decision tree calculates the sum of the weights of the samples. In other words, misclassified samples with a higher sample weight have more impact on finding the best split of a current node in the tree.

For example, for classification task with $C$ classes, the Gini score (or Gini impurity) computes the probabilities $P(c\mid t)$ that a class $c\in C$ appears in node $t$ as the relative frequency of seeing class $c$ in node $t$:

Instead of using the raw counts, AdaBoost computes the weighted probability as:

Because $P(c\mid t)$ is now dominated by the weights rather than the raw count of samples, any data point with a massive weight (a mistake from the previous round) will heavily skew $P(c\mid t)$ toward its own class. This, in turn will affect the final Gini score of a node $t$, which is computed as $Gini(t) = 1 - \sum_{c\in C} P(c|t)^2$. In simple terms, the process of finding the best split of a node in a Decision Tree is now determined by the sample weights. In practice, this typically manifests as:

- isolating high-weight samples in their own leaf node,

- creating a branch that captures a cluster of difficult samples,

- choosing a threshold specifically because it separates a group of high-weight samples from the rest.

So a useful way to think about it is:

Summing up, in ordinary Decision Trees, the split criterion tries to improve purity for as many samples as possible. In AdaBoost, the split criterion tries to improve purity for as much weight as possible.

Weighted Resampling¶

An alternative to modifying the Decision Tree learning algorithm to directly incorporate sample weights into the split criterion is to leave the tree induction process unchanged and instead use the sample weights during data sampling. In this approach, a bootstrap sample is generated by drawing training samples with replacement according to their weights, such that samples with higher weights have a greater probability of being selected multiple times, while samples with lower weights are selected less frequently or may not be selected at all. The resulting bootstrap dataset is then used to train a standard decision tree without any modifications to its impurity measures or split selection procedure. This strategy allows existing tree learning implementations to be reused while still ensuring that the boosting algorithm emphasizes difficult-to-classify samples, since high-weight samples are more likely to appear in the training data presented to subsequent weak learners.

To give an example, let's go back to our example dataset after we updated the weights as a result from training the first learner — where nothing exciting happened since all sample weights initially were the same.

| Weight wi | ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | DEFAULTED |

|---|---|---|---|---|---|

| 0.071 | 1 | 24 | Single | 28,000 | Yes |

| 0.071 | 2 | 45 | Married | 92,000 | No |

| 0.167 | 3 | 31 | Single | 55,000 | Yes |

| 0.167 | 4 | 52 | Divorced | 38,000 | No |

| 0.071 | 5 | 29 | Married | 120,000 | No |

| 0.071 | 6 | 41 | Widowed | 47,000 | No |

| 0.071 | 7 | 22 | Single | 21,000 | Yes |

| 0.071 | 8 | 36 | Married | 75,000 | No |

| 0.071 | 9 | 58 | Divorced | 33,000 | Yes |

| 0.167 | 10 | 27 | Single | 65,000 | Yes |

Now, instead of directly training the next learner on this dataset, we create a bootstrap sample of the same size by sampling the original dataset. The sampling is random but probabilities are proportional to the weights, meaning a sample with a high(er) weight is more likely to be picked than a sample with a low(er) weight. Since we sample with replacement, an individual sample may appear multiple times or not at all in the bootstrap sample. For example, a bootstrap sample for our example dataset might look as follows:

| Weight wi | ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | DEFAULTED |

|---|---|---|---|---|---|

| 0.071 | 1 | 24 | Single | 28,000 | Yes |

| 0.167 | 3 | 31 | Single | 55,000 | Yes |

| 0.167 | 3 | 31 | Single | 55,000 | Yes |

| 0.167 | 4 | 52 | Divorced | 38,000 | No |

| 0.071 | 5 | 29 | Married | 120,000 | No |

| 0.071 | 6 | 41 | Widowed | 47,000 | No |

| 0.071 | 9 | 58 | Divorced | 33,000 | Yes |

| 0.167 | 10 | 27 | Single | 65,000 | Yes |

| 0.167 | 10 | 27 | Single | 65,000 | Yes |

| 0.167 | 10 | 27 | Single | 65,000 | Yes |

Here, ID 3 was picked twice and ID 10 was picked three times since their higher weight made them more likely part of the bootstrap sample. Based on this bootstrap sample, the next learner is not trained, which again results in a Decision Stump, new misclassifications and therefore new weights. Two important details are worth mentioning:

- Each bootstrap sample is generated by drawing from the original dataset (not the previous bootstrap sample).

- The misclassified samples of each learner (i.e., Decision stump) are derived using the original data — that is, we use the bootstrap sample only to train the learner, but we evaluate it using the original dataset, this includes that we always update the weights in the original dataset.

Weighted loss vs. weighted resampling. It is important to point out that these two approaches are not equivalent. Based on the formula for the weighted probability $P(c\mid t)$ we can see that, for example, a sample with weight $w_i = 0.2$ always contributes twice as much as a sample with weight $w_j = 0.1$ during the split search. The influence of the weights is exact and deterministic. In contrast, weighted sampling has a nondeterministic component, meaning that the weights influence the tree only indirectly through the composition of the training sample. For example, a bootstrap sample may look like the original dataset (or other previous bootstrap sample) even though the sample's weights have changed (a lot). A low probability does not mean a zero probability. A useful way to think about it is:

- Weighted Loss: "Treat this observation as if it were worth 10 ordinary observations."

- Weighted resampling: "I will probably show you this observation about 10 times as often as a normal observation."

If the dataset is large and many bootstrap samples are considered, these viewpoints become similar. For a single tree, however, the weighted loss approach is more precise and typically produces lower-variance behavior. It is therefore the default approach of existing implementations. Note that this assumes that the implementation of the base learner requires to support sample weights. For example the DecisionTreeClassifier class, but also other model implementations, of the scikit-learn support sample weights out of the box. This makes implementing AdaBoost on top of these base learner classes quite straightforward. Of course, in practice, you are likely to directly use the AdaBoostClassifier or AdaBoostRegressor classes when already working with scikit-learn.

Making Predictions¶

AdaBoost trains multiple base learners (e.g., Decision Stump), with each subsequent learner focusing on the errors of the previous one; the number of learners is a hyperparameter, say, $K$. This means that after the training, our model consists of $K$ Decision Stumps. To use this model to make predictions, the most important observation is that the different Decision Trees will generally have performed differently with respect to the total error $\epsilon$; note that this includes the training error of each subsequent weak learner does not necessarily go down, and may even go up. Thus, we cannot make predictions based on, for example, a simple majority voting scheme (like in Random Forests).

During inference, we need to take the training accuracy of each weak learner into account. In AdaBoost, this is reflected by the "amount of say" $\alpha$. Recall that a high $\alpha$ value shows that the learner made very few mistakes, and vice versa for low $\alpha$ values. In the case of regression tasks, the final prediction derives from the weighted sum of outputs from all learners, with the weights being the respective $\alpha$ values. If $f_t$ denotes the of $m$-th weak learner, the final prediction is:

For classification tasks, we also give the input to all $t$ weak learners to get $t$ labels. However, instead of going with the majority label, we return the class with the highest amount of say. To illustrate this, assume that we trained an AdaBoost model based on $8$ Decision Stumps $f_1$, $f_2$, ..., $f_8$ on our example dataset (binary classification). During the training, we have computed for each weak learner its amount of say $\alpha_t$. Now let's assume that for a new data sample $x$, the learners $f_1$, $f_3$, and $f_8$ predict "Yes", while all other learners predict "No". The table below presents all the required information.

| Amount of Say | Output | |

|---|---|---|

| $f_1$ | $\alpha_1 = 0.34 $ | $f_1(x)$ = "Yes" |

| $f_2$ | $\alpha_2 = 0.14 $ | $f_2(x)$ = "No" |

| $f_3$ | $\alpha_3 = 1.20 $ | $f_3(x)$ = "Yes" |

| $f_4$ | $\alpha_4 = 0.58$ | $f_4(x)$ = "No" |

| $f_5$ | $\alpha_5 = 0.09$ | $f_5(x)$ = "No" |

| $f_6$ | $\alpha_6 = 0.62$ | $f_6(x)$ = "No" |

| $f_7$ | $\alpha_7 = 0.45$ | $f_7(x)$ = "No" |

| $f_8$ | $\alpha_8 = 0.97$ | $f_8(x)$ = "Yes" |

Since learners $f_1$, $f_3$, and $f_8$ have predicted "Yes", we need to sum $\alpha_1 + \alpha_2 + \alpha_8 = 2.51$ to get the overall amount of say for "Yes". Summing up the remaining $\alpha$ values for all learners that have predicted "No", we get an overall amount of say of $1.88$. This means that, even though the majority of learners predicted "No", the overall amount of say for "Yes" is larger, making this the final prediction.

Notice that during inference, AdaBoost supports the parallelization of the individual learners, even though the training was strictly sequential. This is different compared to the idea of gradient boosting, as we discuss in a moment.

Summary (AdaBoost). AdaBoost improves predictive performance by iteratively focusing on the training samples that are hardest to predict. It does this by assigning a weight to each training sample, where samples that are consistently classified correctly are considered "easy" and receive lower weights, while misclassified or difficult samples receive higher weights. These sample weights are then incorporated into the training process of each subsequent weak learner, causing the learner to pay more attention to difficult cases and less attention to easy ones. By repeatedly reweighting the samples and combining the resulting weak learners into a weighted ensemble, AdaBoost gradually builds a strong predictor that performs well across the entire dataset.

Predicting the Residuals (Gradient Boosting)¶

AdaBoost improves an ensemble by reweighting the training samples, forcing each new learner to focus more on the examples that previous learners found difficult. An alternative approach is gradient boosting, which shifts the focus from the samples themselves to the errors made by the current ensemble. Instead of increasing the weights of misclassified or poorly predicted observations, each new (weak) learner is trained to predict the residuals — the differences between the observed values and the ensemble's current predictions. By repeatedly fitting learners to these residuals and adding their predictions to the ensemble, gradient boosting gradually reduces the overall prediction error and builds an increasingly accurate model, i.e., a strong learner.

Gradient boosting is a family of ensemble learning algorithms that build models by sequentially fitting learners to the errors made by the current ensemble. The most basic member of this family is the Gradient Boosted Machine (GBM), while XGBoost, LightGBM, and CatBoost are advanced extensions that introduce improvements in predictive performance, computational efficiency, scalability, and support for specific data types such as categorical features. Despite their differences, all of these algorithms typically use Decision Trees as their base learners, combining many weak trees into a powerful predictive model.

Gradient Boosting Machine (GBM)¶

Gradient Boosted Machines (GBMs) are an ensemble learning method that builds a strong predictive model by sequentially combining many weak learners, typically decision trees. The process begins with an initial prediction for every training sample, such as the mean target value in regression problems. The residuals, which represent the errors of the current model, are then computed as the difference between the ground-truth values and the model's predictions. A new learner is trained specifically to predict these residuals, thereby focusing on the mistakes made by the existing ensemble.

Once the learner has been trained, its predicted residuals are added to the current predictions, often scaled by a learning rate to control the magnitude of the update. This adjustment reduces the remaining prediction error and improves the model's overall accuracy. The cycle of computing residuals, training a new learner, and updating predictions is repeated iteratively, with each learner correcting the errors of its predecessors. Training continues until a predefined number of learners has been added or another stopping criterion is reached, resulting in a powerful ensemble model that progressively refines its predictions.

Training GBMs¶

Let's use a simple example to illustrate the idea, again using our example dataset of bank customers. Since the computation of residuals is more straightforward for numerical values, we now consider a regression task where the goal is to predict a customer's credit limit in dollars. The table below shows the dataset with all $N=10$ samples.

| ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | LIMIT |

|---|---|---|---|---|

| 1 | 24 | Single | 28,000 | 1,000 |

| 2 | 45 | Married | 92,000 | 1,200 |

| 3 | 31 | Single | 55,000 | 1,400 |

| 4 | 52 | Divorced | 38,000 | 900 |

| 5 | 29 | Married | 120,000 | 1,000 |

| 6 | 41 | Widowed | 47,000 | 600 |

| 7 | 22 | Single | 21,000 | 900 |

| 8 | 36 | Married | 75,000 | 1,100 |

| 9 | 58 | Divorced | 33,000 | 600 |

| 10 | 27 | Single | 65,000 | 1,300 |

For regression tasks, the initial prediction of a Gradient Boosted Machine can, in principle, be any constant value. However, because no information from the features has been incorporated at the start of training, a sensible default is to predict the mean of all target values in the training data. This choice minimizes the overall squared error among all possible constant predictions and therefore provides the best baseline estimate before any learners are trained. Starting from the mean ensures that the subsequent learners focus on explaining the remaining variation in the data by predicting the residuals, which are the differences between the observed outcomes and the current predictions.

For our example dataset, the mean of all target values (i.e. feature LIMIT) is conveniently $1,000$. Thus, if $F_{0}$ denotes our initial model, we have $F_{0}(\mathbf{x}_i) = 1,000$ as the initial prediction for all training samples. For the first learner , we then need to compute the residual $r_{i}^{(1)}$ for a data sample $\mathbf{x}_i$ as the difference between its ground truth $y_i$ and the current prediction; more formally $r_{i}^{(1)} = y_i - F_{0}(\mathbf{x}_i)$. For example, the last sample $\mathbf{x}_{10}$ has a ground truth values of $y_{10} = 1,300$, meaning that after subtracting the initial prediction $F_{0}(\mathbf{x}_{10}) = 1,000$, we get its residual $r_{10}^{(1)} = 300$. The updated table below shows the result after performing this step for all data samples.

| ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | LIMIT $y_i$ | $F_{0}(\mathbf{x}_i)$ | $r_{i}^{(1)}$ |

|---|---|---|---|---|---|---|

| 1 | 24 | Single | 28,000 | 1,000 | 1,000 | 0 |

| 2 | 45 | Married | 92,000 | 1,200 | 1,000 | 200 |

| 3 | 31 | Single | 55,000 | 1,400 | 1,000 | 300 |

| 4 | 52 | Divorced | 38,000 | 900 | 1,000 | -100 |

| 5 | 29 | Married | 120,000 | 1,000 | 1,000 | 0 |

| 6 | 41 | Widowed | 47,000 | 600 | 1,000 | -400 |

| 7 | 22 | Single | 21,000 | 900 | 1,000 | -100 |

| 8 | 36 | Married | 75,000 | 1,100 | 1,000 | 100 |

| 9 | 58 | Divorced | 33,000 | 600 | 1,000 | -400 |

| 10 | 27 | Single | 65,000 | 1,300 | 1,000 | 300 |

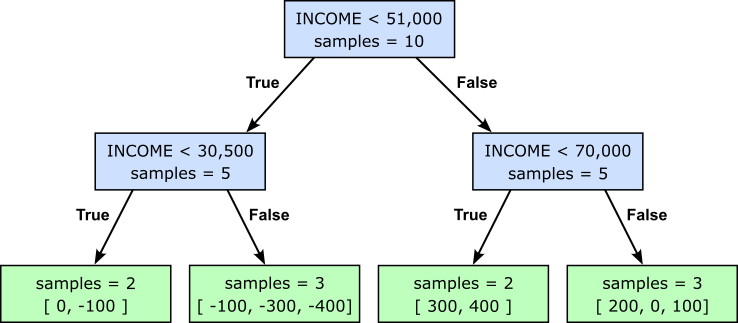

The GBM now trains the first learner $f_1$ with the task to predict the residuals $f_1(\mathbf{x}_i)$ for each training sample $\mathbf{x}_i$. As commonly done, we rely on Decision Trees — more specifically, Decision Stumps since we train weak learners — as the base learner. To keep the example simple and illustrative, let's assume we have trained a Decision Stump with a maximum depth of $2$ and which only considered the feature ANNUAL_INCOME to. Again, this limitation is only to ensure convenient results for the running example. With these consideration, the resulting Decision Stump looks as follows:

In the next step, we use the learner $f_1$ to predict the target values for each data sample. Keep in mind that our learner is a shallow tree (i.e., a Decision Stump), so its predictions are generally the means of all the values within the respective child node. For example, the right-most leaf node contains the residuals for the 2nd, 5th, and 8th sample. The mean of these three residuals is $(200+0+100)/3 = 100$. This means that the prediction for these three sample with respect to learner $f_1$ are $f_1(\mathbf{x}_2) = f_1(\mathbf{x}_5) = f_1(\mathbf{x}_8) = 100$. The table below includes the predicted values for all data samples.

| ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | LIMIT $y_i$ | $F_{0}(\mathbf{x}_i)$ | $r_{i}^{(1)}$ | $f_1(\mathbf{x}_i)$ |

|---|---|---|---|---|---|---|---|

| 1 | 24 | Single | 28,000 | 1,000 | 1,000 | 0 | -50 |

| 2 | 45 | Married | 92,000 | 1,200 | 1,000 | 200 | 100 |

| 3 | 31 | Single | 55,000 | 1,400 | 1,000 | 400 | 350 |

| 4 | 52 | Divorced | 38,000 | 900 | 1,000 | -100 | -300 |

| 5 | 29 | Married | 120,000 | 1,000 | 1,000 | 0 | 100 |

| 6 | 41 | Widowed | 47,000 | 600 | 1,000 | -400 | -300 |

| 7 | 22 | Single | 21,000 | 900 | 1,000 | -100 | -50 |

| 8 | 36 | Married | 75,000 | 1,100 | 1,000 | 100 | 100 |

| 9 | 58 | Divorced | 33,000 | 600 | 1,000 | -400 | -300 |

| 10 | 27 | Single | 65,000 | 1,300 | 1,000 | 300 | 350 |

The last step — well, for this first iteration — is to update our current $F_{0}$ with respect to the predicted residual $f_1(\mathbf{x}_i)$. In general, although this is not guaranteed, samples with current predictions larger than their ground truth values will have positive predicted residuals — recall that we compute $r_{i}^{(1)} = y_i - F_{0}(\mathbf{x}_i)$. As such, to get the current prediction closer to the ground truth, we need to add the current prediction and the residuals, i.e., $F_{1}(\mathbf{x}_i) = F_{0}(\mathbf{x}_i) + f_1(\mathbf{x}_i)$.

However, using the raw predicted residuals would typically cause the learner to make (overly) large corrections. As a result, the ensemble may fit the training data too aggressively, including noise and random fluctuations, which increases the risk of overfitting and poor performance on unseen data. In practice, the model can become unstable, with later learners overcorrecting errors made by previous learners rather than gradually refining the predictions. Thus, instead of adding the raw prediction residuals, GBM introduces a learning rate $\eta$ to scale down the predicted residuals. This gives us the final update rule: $F_{1}(\mathbf{x}_i) = F_{0}(\mathbf{x}_i) + \eta f_1(\mathbf{x}_i)$. Setting $\eta = 0.1$ and applying the rules to our data we get:

| ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | LIMIT $y_i$ | $F_{0}(\mathbf{x}_i)$ | $r_{i}^{(1)}$ | $f_1(\mathbf{x}_i)$ | $F_{1}(\mathbf{x}_i)$ |

|---|---|---|---|---|---|---|---|---|

| 1 | 24 | Single | 28,000 | 1,000 | 1,000 | 0 | -50 | 995 |

| 2 | 45 | Married | 92,000 | 1,200 | 1,000 | 200 | 100 | 1,010 |

| 3 | 31 | Single | 55,000 | 1,400 | 1,000 | 400 | 350 | 1,035 |

| 4 | 52 | Divorced | 38,000 | 900 | 1,000 | -100 | -300 | 970 |

| 5 | 29 | Married | 120,000 | 1,000 | 1,000 | 0 | 100 | 1,010 |

| 6 | 41 | Widowed | 47,000 | 600 | 1,000 | -400 | -300 | 970 |

| 7 | 22 | Single | 21,000 | 900 | 1,000 | -100 | -50 | 995 |

| 8 | 36 | Married | 75,000 | 1,100 | 1,000 | 100 | 100 | 1010 |

| 9 | 58 | Divorced | 33,000 | 600 | 1,000 | -400 | -300 | 970 |

| 10 | 27 | Single | 65,000 | 1,300 | 1,000 | 300 | 350 | 1,035 |

With updating the current prediction, we have completed the first iteration and can now continue with the next iterations using the updated predictions as the starting point; of course, the core steps remain exactly the same. In general, in the $m$-th iteration, we perform the following steps:

- Compute the residuals: $\ r_{i}^{(m)} = y_i - F_{m-1}(\mathbf{x}_i)$

- Fit a weak learner $\ f_m \ $ on residuals

- Compute the predicted residuals $\ f_m(\mathbf{x}_i)$

- Update the current predictions: $\ F_{m}(\mathbf{x}_i) = F_{m-1}(\mathbf{x}_i) + \eta f_m(\mathbf{x}_i)$

To add to our example, the table below shows the results after the second iteration.

| ID | AGE | MARITAL_STATUS | ANNUAL_INCOME | LIMIT $y_i$ | $F_{0}(\mathbf{x}_i)$ | $r_{i}^{(1)}$ | $f_1(\mathbf{x}_i)$ | $F_{1}(\mathbf{x}_i)$ | $r_{i}^{(2)}$ | $f_2(\mathbf{x}_i)$ | $F_{2}(\mathbf{x}_i)$ |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 24 | Single | 28,000 | 1,000 | 1,000 | 0 | -50 | 995 | 5 | -45 | 990.5 |

| 2 | 45 | Married | 92,000 | 1,200 | 1,000 | 200 | 100 | 1,010 | 190 | 90 | 1019.0 |

| 3 | 31 | Single | 55,000 | 1,400 | 1,000 | 400 | 350 | 1,035 | 365 | 315 | 1066.5 |

| 4 | 52 | Divorced | 38,000 | 900 | 1,000 | -100 | -300 | 970 | -70 | -270 | 943.0 |

| 5 | 29 | Married | 120,000 | 1,000 | 1,000 | 0 | 100 | 1,010 | -10 | 90 | 1019.0 |

| 6 | 41 | Widowed | 47,000 | 600 | 1,000 | -400 | -300 | 970 | -370 | -270 | 943.0 |

| 7 | 22 | Single | 21,000 | 900 | 1,000 | -100 | -50 | 995 | -95 | -45 | 990.5 |

| 8 | 36 | Married | 75,000 | 1,100 | 1,000 | 100 | 100 | 1010 | 90 | 90 | 1019.0 |

| 9 | 58 | Divorced | 33,000 | 600 | 1,000 | -400 | -300 | 970 | -370 | -270 | 943.0 |

| 10 | 27 | Single | 65,000 | 1,300 | 1,000 | 300 | 350 | 1,035 | 265 | 315 | 1066.5 |

This process continues until the specified number of learners have been trained; the number of learners is a hyperparameter, and so is the learning rate $\eta$. Keep in mind that getting the predicted residuals $f_m(\mathbf{x}_i)$ requires fitting a learner $f_m$ to the residuals $r_{i}^{(m)}$. The long-term trend of this sequential training of learners is:

- The residual $r_{i}^{(m)}$ will go towards $0$

- The predictions $F_{m}(\mathbf{x}_i)$ will get closer to the true values $y_i$

Important: Note that this behavior describes the long-term trend. Both the residuals and the difference between predictions and true values are generally monotonically decreasing. To give an example, which you may have already spotted, the initial prediction of the first sample already matches the true values of $1,000$. However, the update using the predicted residuals — which is generally the mean of several residuals — causes the prediction to actually deviate from the true value at first.

Like with any boosting strategy, the final output of training a GBM is a sequence of trained based learners $f_1$, $f_2$, ..., $f_K$, typically Decision Stumps, with $K$ being the specified number of learners.

Making Predictions¶

Once a Gradient Boosted Machine has been trained, it makes predictions by following the same sequence of updates that was learned during training. For a new sample $\mathbf{x}$, the prediction is initialized with the same constant value used at the start of training (e.g., $F_{0}(\mathbf{x}_i) = 1,000$ for our running example). The sample is then passed through the first weak learner $f_1$, whose output $f_1(\mathbf{x}_i)$ is added to the current prediction, scaled by the learning rate $\eta$. This process is repeated sequentially for all trained learners in the ensemble. Each learner contributes a small correction to the current prediction, gradually refining it based on patterns it learned from the residuals during training. Mathematically, the prediction $\hat{y}_{i}$ for an unseen sample $\mathbf{x}_i$ is computed as:

Note that, compared to AdaBoost, inference in GBMs is also strictly sequential (not just the training). This is because each learner in a GBM predicts a correction to the current prediction, making the output of one learner a necessary input for the next. Consequently, the learners cannot be evaluated independently and combined afterward; instead, predictions must be updated step by step by traversing the entire sequence of trained learners in order.

GBMs for Classification¶

To outline the idea and the basic steps of Gradient Boosted Machines, we used an example dataset for a regression task to cover the initialization as well as the first two iterations to provide a complete worked example. We chose a regression task since the notions of initial/current predictions as well as of residuals are much more straightforward when dealing with numerical target values (here: dollar values). However, GBMs also support classification tasks, and all the core steps remain exactly the same. While an in-depth discussion is beyond this overview notebook, here are the basic requirements for training a GBM for classification task assuming $C$ different classes:

Initial/current predictions: For each sample, the model GBM starts with a score (e.g., logits or probabilities) for each class, representing the prior belief about the probability of each class before considering any features. For example, assuming a balanced dataset with $4$ classes and using probabilities as scores, each sample will start with an initial prediction $(0.25, 0.25, 0.25, 0.25)$, i.e., a probability of $0.25$ for each class.

Computing residuals: Like before the residuals are computed as the difference between the true values and the current predictions. Again, assuming a classification task with $C=4$, a target vector of $(0, 1, 0, 0)$ for a training sample $\mathbf{x}_i$ indicates that $\mathbf{x}_i$ belongs to Class $2$. Computing the residuals now comes down to subtracting the target vector for the current predictions vector, for example:

Predicting residual: Computing the predicted residuals using the trained learner. Since the residuals are numerical values (and not class labels), the learner will in fact be a regression model (e.g., a Decision Stump regressor as used above). More specifically, given $C$ classes, a GBM will train $C$ regression models in each iteration, one for each class — although alternatives multi-output regression trees are possible. On learner with its $C$ regression models is trained, we use the learner to predict the residual for each training sample. Like before, since the trees are very shallow, the predicted residuals are likely to be the means across several samples. For example, for our training sample $\mathbf{x}_i$ might get the vector of predicted residuals $f_1(\mathbf{x}_i) = (-0.50, 0.70, -0.40, -0.60)$.

Updating model: Using the predicted residual to update the current prediction is done using the same rule: $ F_{m}(\mathbf{x}_i) = F_{m-1}(\mathbf{x}_i) + \eta f_m(\mathbf{x}_i)$. For our example, we can now update the current predictions vector $\hat{y}_{i}^{(1)}$ using the vector of prediction residuals $f_1(\mathbf{x}_i)$, and get:

In short, GBMs and variants/extensions such as XGBoost, LightGBM, and CatBoost, work internally very similarly: they use regression trees regardless of whether the final task is regression or classification. The difference lies not in the type of tree being trained, but in the loss function being optimized and how the residuals are computed. A useful way to think about gradient boosting is:

- GBM for regression: regression trees predict residuals of the target value.

- GBM for classification: regression trees predict residuals of the classification loss.

The main take-away message is that in both cases, the base learners are fundamentally performing regression.

Where is the Gradient?¶

The name Gradient Boosted Machines originates from the idea that each newly trained learner attempts to move the model in a direction that reduces the prediction error. Recall that for both regression and classification tasks, GBM always trains regression models for its learners, since the targets are always numerical values; see above. The standard loss $\mathcal{L}(y_i, \hat{y}_i)$ for a single sample $\mathbf{x}_i$ regression task is the squared error. However, keep in mind that we need to compute this loss each learner $f_m$, which is defined as:

where $\hat{y}_i^{(m)} = F_{m}(\mathbf{x}_i)$, i.e., the output of the model after $m$ iterations. The factor $1/2$ is not important, but it makes the final result more convenient, as we see in a moment. We can no compute the gradient $g_i^{(m)}$ for sample $\mathbf{x}_i$ by computing the first derivative of the loss with respect to the predicted output (here: the predicted residual):

Here we can see the convenience of factor $1/2$. Since we want to reduce the loss, we move in the direction of the negative gradient. We get the negative gradient by multiplying both sides by $-1$, which gives us $y_i - y_i^{(m)}$, which is simply our expression to compute $r_{i}^{(m)}$. This is why the residuals in a regression GBM can be interpreted as the negative gradients of the squared-error loss. Historically, early explanations of boosting often described the algorithm as "fitting the residuals". The more general gradient boosting framework recognizes that what is actually being fitted is the negative gradient of the loss function. For squared-error loss, these two concepts happen to be identical:

Side notes. While the connection between the gradient and the residuals seem rather straightforward, there are some details worth pointing out:

The term gradient is somewhat of a misnomer in the simplified residual-based view of GBMs. In calculus, a gradient describes a continuous rate of change, whereas GBMs update their predictions through a sequence of discrete steps, each represented by a newly trained weak learner. The residuals can therefore be viewed as an approximation of the direction in which the model should move to reduce the error, rather than a true gradient in the mathematical sense. This interpretation becomes more accurate in the general formulation of gradient boosting, where learners are fitted to the negative gradient of a chosen loss function, but the updates themselves remain discrete additions of weak learners.

To be more technically correct, $r_{i}^{(m)}$ is called the pseudo-residual because $r_{i}^{(m)}$ is only the true residual $y_i - \hat{y}_i^{(m)}$ for the squared error loss. This changes for different loss / error functions. For example, if we would use the absolute error (L1 loss) where $\mathcal{L}^{(0)} = |y_i - \hat{y}_i^{(0)}|$ to be more robust against outliers, the negative gradient changes to:

Summary. Gradient Boosted Machines (GBMs) are based on the fundamental idea of building a strong predictive model by sequentially combining many weak learners, typically decision trees. Starting from an initial prediction, each learner is trained to correct the errors of the current model by predicting residuals or, more generally, the negative gradients of a chosen loss function. The predictions are then updated iteratively, allowing the ensemble to gradually improve its performance. This stage-wise learning process enables GBMs to model complex relationships while maintaining relatively simple individual learners.

This core boosting principle forms the foundation of many modern gradient boosting frameworks, including XGBoost, LightGBM, and CatBoost. While these frameworks introduce additional innovations such as second-order optimization, regularization, specialized handling of categorical features, improved treatment of missing values, and highly optimized training procedures, they all retain the central idea of iteratively adding learners that reduce the remaining prediction error. As a result, understanding the basic mechanics of GBMs provides the conceptual basis for understanding these more advanced and widely used boosting algorithms.

XGBoost¶

XGBoost (eXtreme Gradient Boosting) is one of the most popular and widely used boosting frameworks in machine learning. It builds upon the fundamental ideas of Gradient Boosted Machines (GBMs), which iteratively train weak learners to correct the errors of the current model, while introducing several enhancements that improve both predictive performance and computational efficiency. As a result, XGBoost has become a standard choice for many machine-learning competitions and real-world applications, particularly for structured tabular data.

The two most important extensions introduced by XGBoost are the use of Newton's method and regularization. While traditional GBMs rely only on first-order gradient information, XGBoost additionally incorporates second-order derivative information, allowing it to make more informed optimization steps and often converge faster. Furthermore, XGBoost explicitly regularizes the complexity of the learned trees, helping to reduce overfitting and improve generalization. Beyond these core innovations, XGBoost includes numerous practical improvements, such as automatic handling of missing values, row and feature subsampling, tree pruning, and a highly optimized implementation that enables efficient training on large datasets. Together, these enhancements make XGBoost both more powerful and more scalable than traditional GBMs.

The following sections aim to provide the intuition and explain the basic concepts behind these improvements that XGBoost makes to GBMs; again, a deep dive into XGBoost is beyond the scope of this overview notebook.

Newton Boosting¶

We just saw how GBMs use the first-order derivative (i.e., the gradients) to find the residuals (i.e., the direction of the error). Using only the first-order derivative (the gradient) provides information about the direction in which the loss function is increasing or decreasing, but it does not indicate how quickly the slope itself is changing. As a result, optimization steps may be too large in regions where the loss function is steep or too small in flatter regions, leading to slower convergence or less accurate updates.

XGBoost uses Newton Boosting, which itself is based on Newton's method, a general optimization algorithm that uses both the first and second derivatives of a function to find a minimum or maximum. Newton Boosting applies the idea of Newton's method within the gradient boosting framework. Instead of fitting learners to the negative gradient alone (as in traditional gradient boosting), it uses both the gradient and Hessian (second derivative) information when training the learners. The second-order derivative captures the curvature of the loss function and therefore provides information about the local shape of the optimization landscape. By incorporating both the gradient and the curvature, Newton's method can estimate not only the direction but also the appropriate magnitude of an update, allowing XGBoost to make more effective optimization steps and often converge faster than methods based solely on first-order information.

Let's see how this looks like for the squared error loss $\mathcal{L}(y_i, \hat{y}_i) = \frac{1}{2}\left(y_i -\hat{y}_i \right)^2$ for a training sample $\mathbf{x}_i$. Well already know that the negative gradient $-g_i$ for $\mathbf{x}_i$ is:

Now, the second-order derivative, or the Hessian $h_i$, for sample $\mathbf{x}_i$ is defined as

In short, for the standard squared error loss, the Hessian is simply $h_i = 1$, meaning that every training sample contributes equally to the second-order information used by XGBoost. However, for other loss functions the Hessian may vary from sample to sample and depends on the current prediction. In these cases, the Hessian provides additional information about the local curvature of the loss function, allowing XGBoost to adapt the magnitude of its updates based on how sensitive the loss is to changes in the predictions.

Recall that each boosting iteration first requires to compute the residual (or rather the pseudo-residual). XGBoost is computing the residuals exactly as traditional GBMs: the difference between the current predictions and the true values. In other words, for computing the residuals, XGBoost uses only the gradient $g_i$ (i.e., the first-order derivative information). So far, XGBoost and GBMs behave the same. The Hessian $h_i$ (i.e., the second-order derivative information) is used for training the learner and computing the predicted residual. To show how this works, we first need to talk about regularization, the other core concept the XGBoost introduces to GBMs.

Regularization¶

Regularization is a technique used to reduce overfitting by discouraging overly complex models that fit not only the underlying patterns in the training data but also noise and random fluctuations. It does so by introducing a penalty for model complexity into the optimization objective, for example by limiting the magnitude of model parameters or the complexity of decision trees. As a result, regularization often improves a model's ability to generalize to unseen data, leading to better predictive performance in practice.

A basic GBM controls overfitting primarily through heuristics such as limiting tree depth (i.e., "manually" enforcing shallow trees through hyperparameters), tuning the learning rate $\eta$ (shrinkage), or subsampling data. In contrast, XGBoost explicitly integrates the concept of regularization — together with the gradient and Hessian information — into both the training and the prediction of residuals. Since these require some nontrivial extension to traditional GBMs, to focus here is to provide a basic intuition.

Let's start with the training. Recall when training a learner (i.e., Decision Tree/Stump) for a class GBM, the "only" goal is to minimize the overall loss $\mathcal{L} = \sum_{i=1}^{n} \mathcal{L}(y_i, \hat{y}_i)$, with $n$ being the total number of training samples. Trying to optimize this objective leads to the classic approach of finding the best splits using criteria such as the Mean Squared Error (MSE) or the Sum of Square Errors (SSE). Of course, optimizing this loss alone would result in strong learners and increase the risk of overfitting. This is why, when using GBMs, restricting the complexity of the trees using hyperparameters (e.g., the maximum depth of a tree, or the minimum number of samples to split a tree) is required.

In contrast, XGBoost uses regularization to automatically implement constraints on the complexity of the trained tree. The model does so by considering the following objective function:

where $\Omega(f_k)$ is the regularization term for the $k$-th tree in the sequence. For any tree $f$, this regularization term is defined as:

where:

- $T$ is the number of leaves in the tree

- $w_j$ is the prediction value stored in leaf $j$

- $\gamma$ is a penalty factor for each additional leaf

- $\lambda$ is the L2 regularization parameter

Intuitively, the first term $\gamma T$ discourages unnecessarily large trees by charging a cost for every leaf, and the second term $\frac{\lambda}{2}\sum_{j=1}^T w_j^2$ discourages extreme leaf predictions by shrinking leaf values toward zero. Regarding the latter, remember that we predict residuals, meaning that extreme predictions correspond to aggressive corrections when we update the current predictions — which we want to avoid to reduce the risk of overfitting! By penalizing large leaf values through the regularization term, XGBoost encourages the model to make more conservative updates.

Side note: Although XGBoost incorporates regularization to control model complexity and reduce overfitting, it still relies on hyperparameters such as the maximum tree depth, minimum child weight, and learning rate. Regularization penalizes overly complex trees, but it does not completely determine the structure of the model. Hyperparameters provide additional control over how the trees are grown and how aggressively the ensemble learns, allowing practitioners to balance predictive accuracy, computational efficiency, and generalization performance for a given dataset.

During a boosting iteration, at iteration $m$, when a new tree $f_m$ is added, the objective for this step is:

Directly optimizing XGBoost's objective function within a decision tree is mathematically challenging because the tree structure introduces discrete decisions, such as selecting split points and assigning observations to leaves. These decisions make the objective function non-differentiable and difficult to optimize analytically. To overcome this challenge, XGBoost approximates the loss function using a second-order Taylor expansion, transforming the original optimization problem into a simpler form that can be optimized efficiently when constructing the tree. Skipping the mathematical details here, equation for approximating the loss $\tilde{\mathcal{L}}^{(m)}$ is:

Firstly, notice that this approximation now incorporates both the gradient $g_i^{(1)}$ as well as the $f_i^{(m)}$, i.e., both first-order and second-order derivative information. More importantly, the mathematical convenience of the second-order Taylor expansion is that it transforms an arbitrary, potentially messy loss function into a clean, predictable quadratic expression in $f_t(\mathbf{x}_i)$. A quadratic function is the ultimate convenience tool in optimization because its properties are thoroughly understood and exceptionally easy to solve analytically.

Let's remind ourselves that $f_t(\mathbf{x}_i)$ is the predicted values for training sample $\mathbf{x}_i$, and this is the same value for all samples ending up in the same leaf of the $m$-th learner. Suppose a leaf $j$ predicts a constant value $w_j$ for all samples in that leaf, then $w_j = f_m(\mathbf{x_i})$ for all $\mathbf{x}_i$ where $i\in I_{j}$, and $I_j$ are the set of indices in leaf $j$. With that, we can express the $\tilde{\mathcal{L}}^{(m)}$ as the sum over the losses for all $T$ leaves. After some additional algebraic transformation, we get the following expression:

If we denote the sum of all gradients as $G_j^{(m)} = \sum_{i\in I_j} g_i^{{(m)}}$ and the sum of all Hessians as $H_j^{(m)} = \sum_{i\in I_j} h_i^{{(m)}}$, we can simplify the expresssion:

where $\mathcal{L}_j^{(m)}$ is the loss for leaf $j$.

Now, to optimize the approximated objective function, XGBoost must determine the best prediction value $w_j$ for each leaf. Since $w_j$ is the quantity that directly controls the leaf's contribution to the model's predictions, the objective can be viewed as a function of $w_j$. Taking the derivative with respect to $w_j$ measures how the objective changes when the leaf prediction is adjusted slightly. The optimal value of $w_j$ occurs at a minimum of the objective, where the slope is zero. Therefore, setting the derivative equal to zero allows XGBoost to find the leaf weight that minimizes the loss while accounting for regularization. Computing this derivatives gives us:

Note that all sum terms for leaves that are not leaf $j$ as well as the term $\gamma T$ do not depend on $w_j$ and are therefore considered constants when deriving the expression with respect to $w_j$. Setting the derivative to $0$ and solving for $w_j$ gives us the optimal value $w_i^{\ast}$:

Notice that the regularization parameter $\lambda$ is in the denominator. As $\lambda$ increases, the magnitude of $w_j$ shrinks toward zero. Intuitively, this makes the model more conservative by preventing individual leaves from making overly large corrections based on limited or noisy data. This is desirable because large leaf weights can lead to overfitting, where the model captures random fluctuations in the training data rather than genuine patterns.

Side note: Assuming the standard squared error with the Hessian $h_i^{(m)} = 1$, $H_j^{(m)}$ simplifies to $n_j^{(m)}$ being the number of samples in leaf $j$. Further, if we would set $\lambda = 0$, the expression for simplifies to the mean overall gradients $G_j^{(m)}$, which is exactly the value we get when using a traditional GBM.

We can now compute the minimal loss $\mathcal{L}_j^{(m)}$ for leaf $j$ by plugging the expression for $w_i^{\ast}$ back into the expression for $\mathcal{L}_j^{(m)}$:

By substituting the optimal leaf weight back into the approximated objective function, XGBoost obtains a measure of the contribution of each leaf to reduce the overall loss. This result can then be used to directly derive a splitting criterion that evaluates whether dividing a node into two child nodes leads to a sufficient improvement in model performance — which omit here to derive in full detail. During tree construction, candidate splits are compared based on the reduction in the objective function they achieve. Importantly, the splitting criterion includes the regularization parameter $\gamma$, which imposes a penalty for creating additional leaves. As a result, a split is only accepted if its improvement outweighs the increase in model complexity, helping to prevent overfitting and produce more compact trees.

Other Improvements¶

Beyond Newton Boosting (second-order optimization) and explicit regularization, XGBoost introduced several important innovations that made it substantially more effective and scalable than traditional GBMs:

Row & column subsampling: Similar to Random Forests, each tree is trained on a random subset of samples (bagging) and random subset of features (feature sampling). The goals is to introduce diversity among trees and make the less correlated to improve robustness, especially in high-dimensional datasets.

Sparsity-Aware learning: XGBoost is designed to efficiently handle sparse data and missing values. During training, it automatically learns the optimal direction for missing values at each split. This avoids the need for explicit imputation and allows the algorithm to exploit information contained in missingness patterns.

Parallelized split computation: While boosting itself remains sequential, XGBoost parallelizes the search for the best split within a tree. The intuition is that evaluating many candidate splits is computationally expensive, so distributing this work significantly speeds up training on large datasets.

Weighted quantile sketch: XGBoost uses an approximate algorithm to identify promising split points without examining every possible threshold. The intuition is that a carefully chosen approximation can dramatically reduce computation while maintaining nearly the same predictive performance.

Out-of-core computation: XGBoost can train on datasets that are too large to fit entirely into memory by processing data in blocks. The intuition is that model performance should not be limited by available RAM, enabling boosting on much larger datasets.

Taken together, these innovations address three key limitations of traditional GBMs: overfitting (shrinkage, subsampling), computational efficiency (parallelization, approximate split finding), and scalability/robustness (sparsity-aware learning, out-of-core computation).

Summary (GMBs vs XGBoost): XGBoost builds upon the foundation of traditional Gradient Boosted Machines (GBMs) by introducing a range of innovations that improve both predictive performance and computational efficiency. Most notably, it employs Newton boosting, which leverages both first- and second-order derivatives of the loss function, and incorporates explicit regularization to control model complexity and reduce overfitting. In addition, XGBoost introduces techniques such as row and feature subsampling, optimized split selection based on a regularized objective, efficient handling of missing and sparse data, and parallelized tree construction. The table below outlines the core differences between traditional GBMs and XGBoost.

| Aspect | Traditional GBM | XGBoost |

|---|---|---|

| Optimization Approach | Fits trees to the residuals (first-order gradients) of the current ensemble. | Uses both gradients and Hessians (second-order information) through Newton boosting. |

| Objective Function | Focuses primarily on reducing prediction error. | Optimizes a regularized objective that balances prediction error and model complexity. |

| Regularization | Relies mainly on hyperparameter tuning (e.g., tree depth, learning rate) to control complexity. | Incorporates explicit regularization terms that penalize complex trees and large leaf weights. |

| Split Selection | Chooses splits based on their ability to reduce prediction error. | Chooses splits based on their improvement to the regularized objective function. |

| Leaf Predictions | Typically based on averages of residuals within a leaf. | Derived analytically from gradients, Hessians, and regularization terms. |

| Overfitting Control | Primarily controlled through shrinkage and tree constraints. | Controlled through both shrinkage and explicit regularization. |